If central banks don’t lance the QE boil now they probably never will, risking soaring inflation that takes the world back to the 1970s

Countries making up three quarters of global economic output have reached critical vaccination thresholds. Many others have largely covered the most vulnerable cohorts.

The world economy is not going back into a collective lockdown whatever the delta variant may bring. Just as the vaccines have broken the link between cases and death, societies have broken the link between the virus and economic loss. Each wave has a diminishing impact.

Fiscal and monetary largesse in the advanced states overwhelm the residual pockets of damage in the OECD bloc. Pent-up savings and a capex restocking cycle should pick up the baton as state support fades (the US fiscal impulse turns negative this quarter).

The UK is the world’s laboratory for opening up. Unfortunately it has done so with breathtaking incompetence and given the process a bad name.

The error is not the decision to lift curbs. It is a legitimate strategy to open up fully during the peak of summer when 70pc of adults have been fully vaccinated. In a sense it is the original (premature) Vallance strategy of letting the virus run in a controlled fashion to achieve herd immunity, but this time in plausible circumstances. The death rate has fallen to levels that resemble winter flu.

It will soon become clear to market traders across the globe whether British hospitalisations will remain manageable or whether the pandemic again approaches the catastrophism of Professor Neil Ferguson. If the latter, Monday’s rush into the safe-haven bonds – gilts, US Treasuries, Bunds – is indeed the harbinger of something serious.

My own view is that the Ferguson sell-off – most visible in crumbling travel stocks, and a 7pc crash in crude priceslinked to jet fuel demand – is to blame the wrong culprit. Commentators are latching onto Covid to explain financial ructions that have their roots elsewhere.

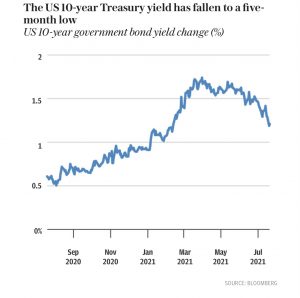

What we really have is a taper tantrum. The Anglo-Saxon central banks have been shocked by the force of the inflation surge and are suddenly turning hawkish in a belated effort to restore their own credibility. The bond markets are pricing in the risk that they will overtighten. This is the “policy error” narrative. Hence the fall in 10-year US yields to 1.2pc, a recession warning.

Every time the US Federal Reserve in particular has tried to extricate itself from the great QE experiment, it has set off bond market turmoil. The attempt in late 2018 to unwind QE by “automatic pilot” led to a plunge in yields and a major Wall Street scare. The Powell Fed was forced to retreat.

The financial system has become acutely sensitive to slight tweaks in monetary policy. This is known as the central bank “debt trap”. The Economic Affairs Committee of the House of Lords alluded to this in its report last week – quantitative easing: a dangerous addiction?

“No central bank has managed successfully to reverse its asset purchases over the medium to long-term, and the key issue as they look to halt or reverse quantitative easing is whether it will trigger panic in financial markets that spills over into the real economy,” it concluded.

This blistering report is key to understanding the market events unfolding. It implicitly accuses the Bank of England’s Governor Andrew Bailey and fellow rate-setters of falling captive to political masters, letting rip on inflation, and playing fast and loose with the credibility of British monetary management.

The Bank knew this damning indictment was coming. It is an open secret that former Governor Mervyn King was the éminence grise behind the drafting. There are few precedents for such a rebuke from the heart of the British establishment. It helps explain why the Monetary Policy Committee has changed its tune so precipitously.

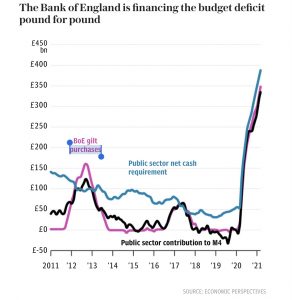

The Lords report strongly suggests that the Bank has been soaking up Treasury debt issuance pound for pound over the last 15 months at the behest of the Government, flirting with Latin American fiscal dominance.

The report said the Bank had failed to offer a scientific justification for what it is trying to achieve with QE, or for why it is continuing to purchase bonds à outrance when the economy is recovering briskly, the housing market is on fire, and inflation keeps overshooting the Bank’s forecasts.

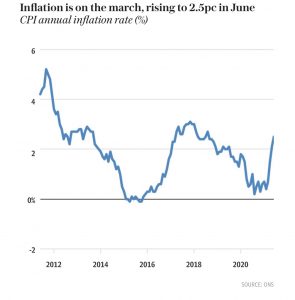

Whether it is due to the wrath of the Lords or the hard data, the Bank is finally tacking hard. Deputy governor Sir David Ramsden last week broached the subject of early bond tapering, confessing that he “wouldn’t be surprised” if inflation hit 4pc later this year. The MPC’s Michael Saunders suggested that a total halt to bond purchases over the next month or two might be a good idea.

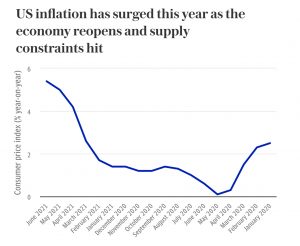

A variant of this hawkish turn is underway in the US, where core inflation is at a 30-year high of 4.5pc and the Fed’s regional presidents are in simmering revolt against the ivory tower New Keynesians at the board in Washington.

The hawks are questioning how the Fed can justify buying $120bn of bonds each month when the National Association of Realtors’ existing home price index is rising at 24pc rate (double the subprime peak), the Biden Administration is running a $3 trillion fiscal deficit equal to 15pc of GDP, and the output gap has closed.

The bond markets are still buying the line that the inflation spike is a transitory distortion caused by Covid reopening. Monetarists say they are reading from an outdated script, unable to see that the secular 40-year slide in inflation has run its course.

I think the monetarists will be proved more right than wrong in this episode and stick to my view that the 32pc increase in the broad US money supply since the start of the pandemic (much of it still unspent) will power this economic expansion for another 12 months at least, probably with a nose-bleed correction along the way.

As the Lords’ report makes clear, not all QE is the same. The post-Lehman blitz occurred when the banking system was broken. Had there been no QE, the broad money supply would have contracted violently and caused a depression. It was also a time of fiscal austerity across the developed world – the greatest collective policy mistake so far this century.

Neither condition prevails today. The US banks are in rude good health. Western governments have concluded that the pauperisation of the bottom half is the greatest threat to democracy and are prepared to spend whatever it takes to restore popular consent. “We have an escalating inflation rate because the state has nationalised the credit creation process and co-opted the central banks in support of their endeavours,” said Peter Warburton from Economic Perspectives.

The Bank of England also propagated this myth in the early days of QE, explicitly stating in a report that bond purchases were the functional equivalent of printing money. This free lunch narrative was not true and is now coming back to haunt us.

In reality, QE as conducted is an asset swap from a long maturity to a short maturity. The greater the stock of bond purchases – soon to be 40pc of GDP – the greater the risk for the Bank of England since it pays interest at Bank rate on excess reserves (as a side-effect of QE) to the commercial banks. The Treasury indemnifies the Bank for losses.

Each one percentage point rise in the rate costs the state £20bn or 0.8pc of GDP. Continuing to conduct QE into an inflationary storm is therefore anything but cost-free. It is akin to a future tax. “We are concerned that if inflation continues to rise, the Bank may come under political pressure not to take the necessary action to maintain price stability,” said the Lords’ report.

Central banking is at a critical juncture. If the Bank of England, the Fed, and their peers do not lance the QE boil now, they probably never will. Inflation will be allowed to take hold and the world will be back to the 1970s. Markets are having great difficulty deciding which of these two outcomes is more likely.